Why Trying to Avoid Every Market Crash Often Leads to Bigger Losses

Most investors dream of doing two things:

Sell before the crash.

Buy before the rebound.

If achieved consistently, this would seem like the ultimate investing strategy.

Yet reality—and mathematics—suggest otherwise.

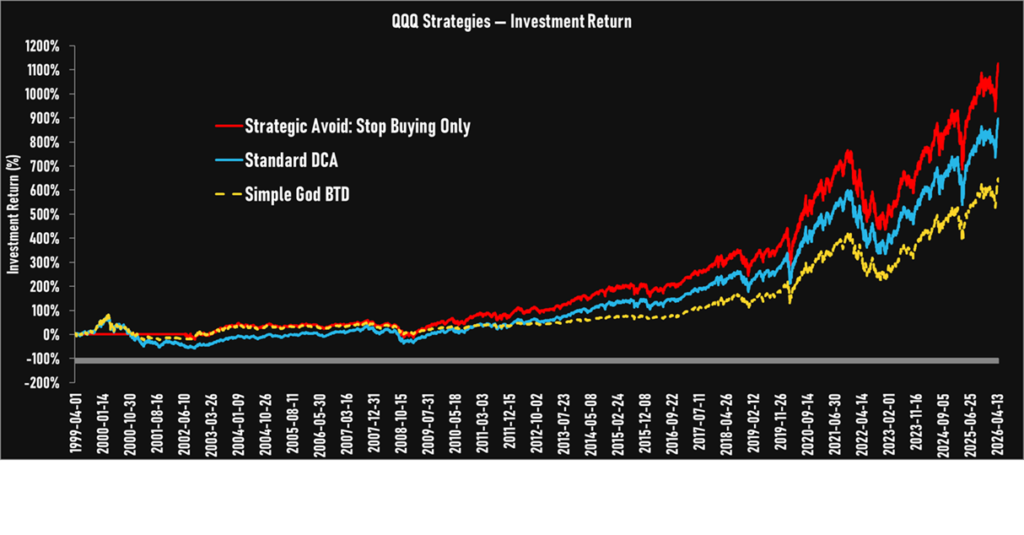

A study comparing different investment approaches on the Nasdaq-100 ETF (QQQ) from 1999 through 2026 reveals a surprising conclusion:

even with perfect hindsight, buying the dip alone does not necessarily outperform a simple dollar-cost averaging strategy.

What truly creates extraordinary returns is something far more difficult—

successfully avoiding major drawdowns while still having the conviction

to buy when fear is at its peak.

The Three Strategies

To evaluate this hypothesis,

we analyzed the performance of the Nasdaq-100 ETF (QQQ) over the following period:

April 1, 1999 – April 30, 2026

Imagine three hypothetical investors:

- Standard DCA (Dollar-Cost Averaging ), investing a fixed amount every month regardless of market conditions.

- Simple God BTD (Buy the Dip), this investor waits patiently and deploys cash only at the exact lowest point between two market highs. In other words, they buy every dip perfectly.

- Strategic Avoid : Stop Buying Only, whenever a future decline exceeding 20% is about to occur, they stop investing entirely, hold cash during the downturn, and then invest at the precise bottom before the recovery begins.

To isolate the effect of timing, none of the investors are allowed to sell.

They can only buy and hold.

The results are counterintuitive.

Perfect dip-buying alone struggles to beat regular DCA.

Only the investor who both avoids large drawdowns and buys near the bottom significantly outperforms.

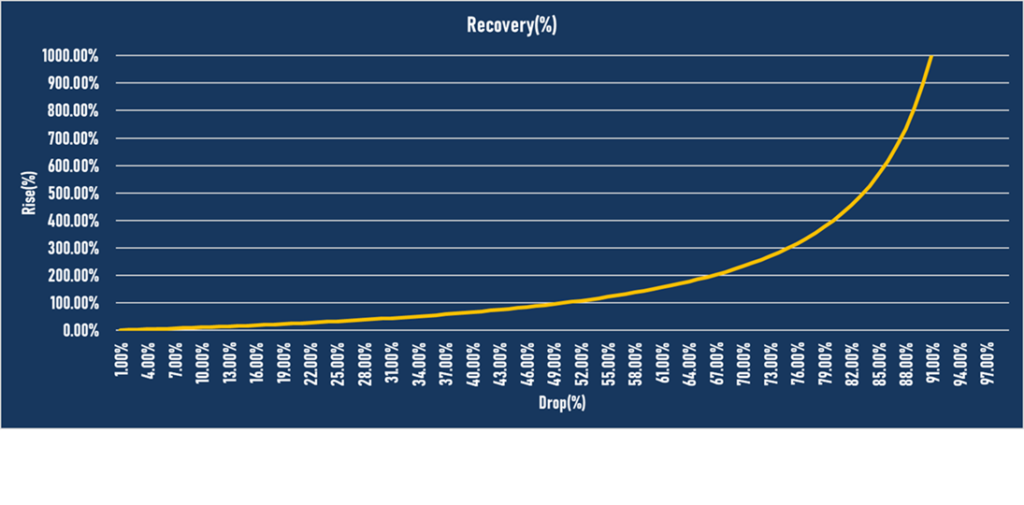

The Mathematics of Losses Is Brutal

The explanation lies in a fundamental property of compounding that many investors underestimate.

Market gains and losses are not symmetric. Consider what it takes to recover from a loss:

• Down 20% → Need +25% to break even

• Down 50% → Need +100%

• Down 75% → Need +300%

• Down 90% → Need +900%

• Down 95% → Need +1,900%

• Down 98% → Need +4,900%

Losses and gains are not symmetrical.

The deeper the loss, the MUCH steeper the climb back.

This asymmetry means that avoiding catastrophic losses can have an outsized impact on long-term returns.

From a mathematical perspective,

• Lose 50%, then gain 100%: You are right back to break-even.

• Dodge the 50% drop, then catch the 100% rally: Your portfolio instantly doubles.

This highlights how devastating drawdowns are to long-term compounding.

If you could sidestep them perfectly, your returns would naturally look spectacular.

The investor who sidesteps a major drawdown preserves capital that does not need to spend years recovering.

This principle is deeply rooted in portfolio theory and risk management.

Warren Buffett’s famous rule—”Never lose money”—is not literally achievable,

but it reflects a profound truth: protecting capital is often more important than maximizing gains.

The Hidden Problem: Avoiding Losses Is Not Enough

At this point, avoiding crashes sounds like the obvious solution.

But there is a catch.

If avoiding declines were all that mattered,

the best strategy would simply be to stay in cash forever.

Clearly, that does not lead to wealth creation.

As the legendary André Kostolany put it:

“If you don’t own wheat when its price falls, you won’t own wheat when its price rises.”

Dodging the crash is useless if you lack the balls to buy the blood.

This is the trap of John Templeton’s famous maxim:

“Bull markets are born on pessimism, grow on skepticism, mature on optimism, and die on euphoria.”

When you are excited to “buy the dip,” it’s not true pessimism yet—the bottom is lower than you think (remember 2008).

By the time the market actually bottoms out, you’ll freeze, calling the initial rally a “dead cat bounce.”

By the time you find your courage, the train has already left the station.

The Best Days Arrive When Nobody Wants Them

Perhaps the strongest argument against market timing comes from a well-documented statistical phenomenon.

A tiny fraction of trading days account for a disproportionate share of long-term returns.

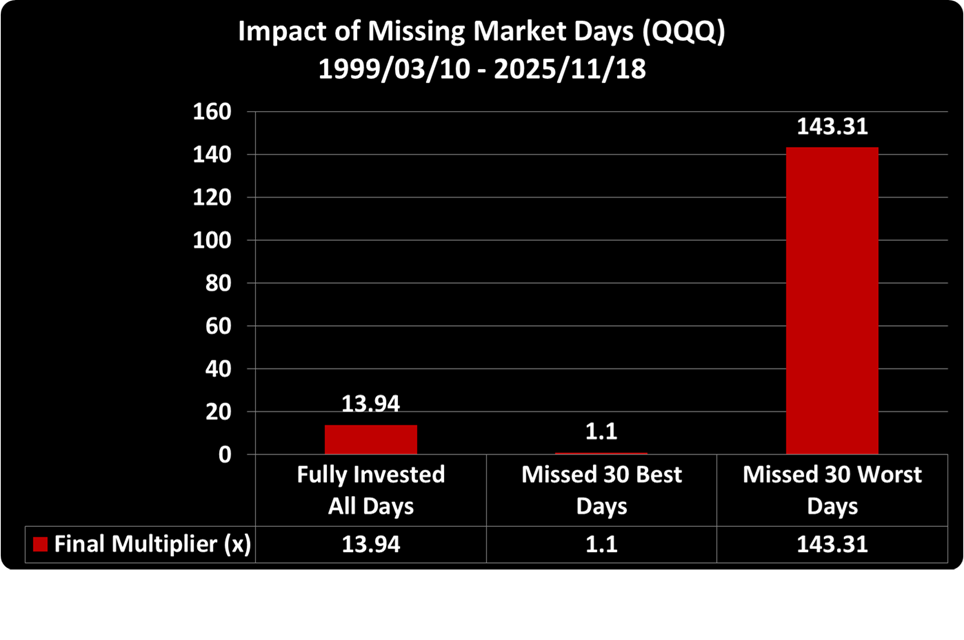

Look at the real-world data for QQQ (Nasdaq-100 ETF) over a 26-year,

8-month horizon (March 1999 – November 2025):

- The Full Ride (Stayed Invested): Turned your initial capital into 13.94x.

- The Market-Timer’s Penalty (Missed the 30 Best Days): Plummets your return to just 1.1x.

- The Oracle’s Dream (Avoided the 30 Worst Days): Rocketed your portfolio to a staggering 143.31x.

This resembles a classic Pareto distribution, where a small percentage of events drives the majority of outcomes.

Yes, I get it.

Sidestepping the worst days yields jaw-dropping returns.

But don’t forget the golden rule we established earlier: blessings and curses walk hand in hand.

In the real world, the worst days and the best days are violently clustered together.

When you actively try to dodge the worst days,

you are almost guaranteed to miss the best ones too.

The challenge is that these exceptional days rarely arrive when investors feel confident.

They often occur:

- Immediately after severe declines

- During periods of extreme uncertainty

- When headlines remain overwhelmingly negative

- Before economic conditions visibly improve

In other words,

the moments when investors most want to stay on the sidelines are often the moments that generate the highest future returns.

Markets reward investors not merely for avoiding risk, but for accepting risk when others are unwilling to.

The Real Lesson

The popular investing fantasy is not buying the bottom.

It is buying the bottom after perfectly avoiding the decline.

The problem is that both decisions require accurate forecasts about the future,

and both must be correct simultaneously.

Missing either side of the equation can dramatically reduce performance.

You may successfully avoid a 30% drawdown only to miss a subsequent 60% rally.

You may jump over a small puddle and fall into a much deeper lake.

This is why simple strategies such as dollar-cost averaging remain remarkably difficult to beat in practice.

Their strength does not come from predicting the future.

It comes from eliminating the need to predict it.

As Peter Lynch famously remarked:

“Far more money has been lost by investors preparing for corrections,

or trying to anticipate corrections, than has been lost in the corrections themselves.“

The greatest challenge in investing is not identifying market bottoms.

It is remaining invested long enough to benefit from the market’s relentless tendency to recover.

Leave a Reply